Buy Now, Pay Later May Trigger America's Next Financial Crisis

How 4 Interest-Free Installments Could Break the Economy

Money & Markets | Volume 1 • No. 1

America didn’t kick its debt addiction after the 2008 financial crisis; it simply found a new drug dealer.

Twenty years ago, banks convinced millions of Americans they could afford homes they couldn’t afford. Today, fintech companies are convincing people they can afford almost everything else. Using debt to live beyond one’s means is as American as the “dream” itself.

Every generation has its financial drug of choice. Ours comes disguised as a sleek, pastel-colored checkout button, and “4 interest-free installments”. The pitch sounds harmless. The consequences may not be. We are once again confusing access to credit with affordability. And history has a nasty habit of repeating itself when we forget that distinction.

The Wild, Wild West of the Early 2000’s

Every financial crisis begins with a lie people desperately want to believe. In the early 2000s that lie was simple: home prices only go up. If houses always increased in value, why worry about whether borrowers could actually repay their loans?

Suddenly everyone seemed to be buying homes and flipping properties. Many had poor credit, little savings, and no realistic path to repayment. Traditionally, those borrowers, known as subprime borrowers, had limited access to mortgages.

Banks changed the rules. Income verification disappeared. Down payments shrank. Loan structures became increasingly creative. Some mortgages even delayed principal payments for years, or what I call “borrow now, pay later” mortgages. The illusion of affordability fueled a housing boom as subprime mortgage originations exploded from $35 billion in 1994 to $600 billion in 2006, representing 5% and 20% of all mortgages, respectively.

Banks made billions lending money to people who couldn’t afford to borrow. What could have possibly gone wrong? By the summer of 2007, the world had its answer.

The New Wild, Wild West

Today’s lending boom doesn’t revolve around houses. It revolves around everyday life. And the money isn’t coming from banks, but fintech companies.

Buy Now, Pay Later has transformed borrowing from a major financial decision into a routine part of shopping. Consumers now finance everything from laptops and airline tickets to DoorDash orders, groceries, and even rent. Some platforms are beginning to offer installment payments for sending money to friends and family.

Think about how crazy that is.

Cash forces you to feel the cost of your decisions. Credit delays the pain. Buy Now, Pay Later attempts to erase the pain altogether. That’s exactly why it’s so dangerous.

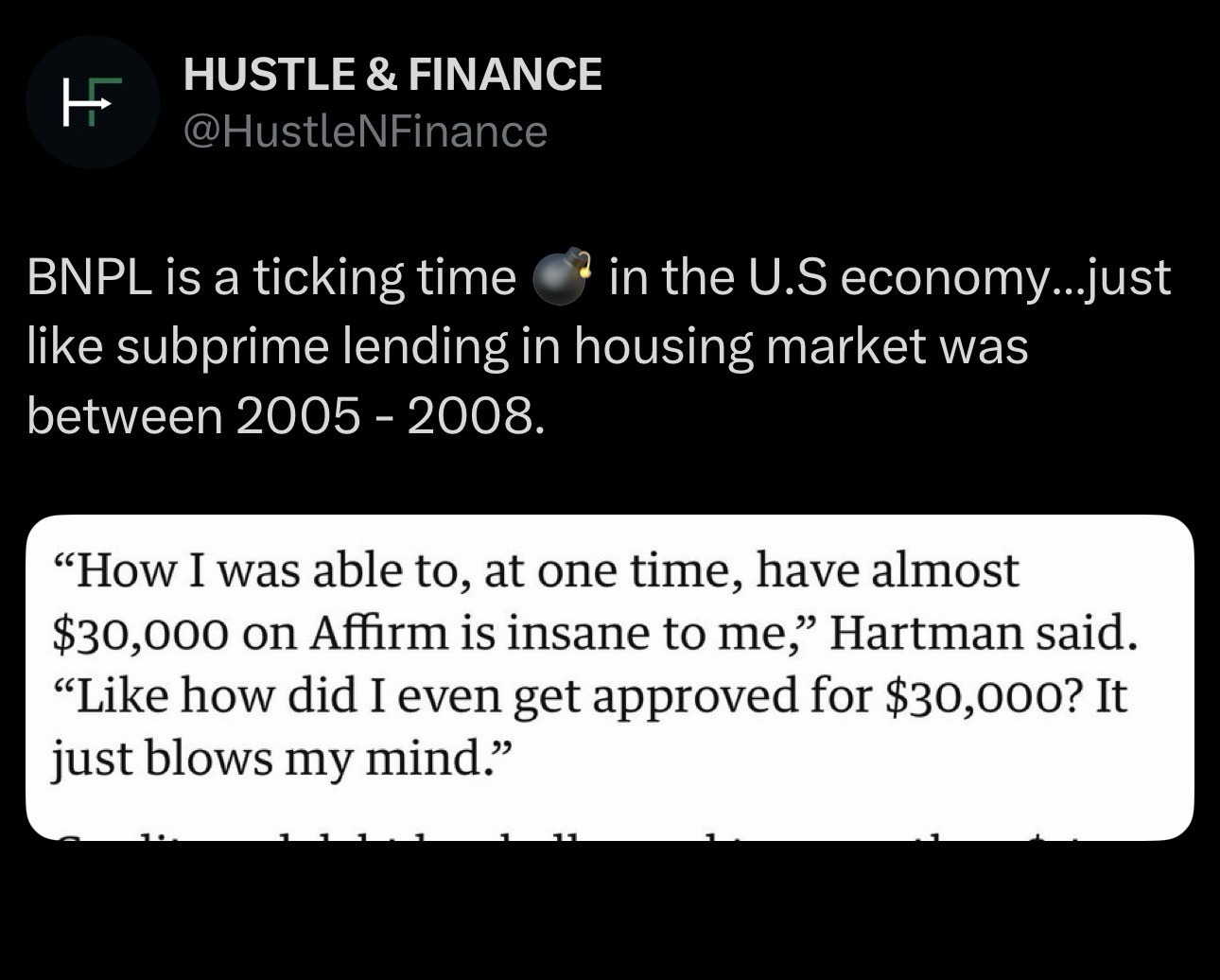

The BNPL industry has exploded into a market estimated to be $560 billion in 2025 with projections approaching $900 billion by the end of the decade. The industry’s growth isn’t being driven by wealthy households paying strategically. It’s increasingly driven by younger consumers already carrying student loans, record credit card balances, facing rising living costs, and with poor credit scores (borrowers with FICO scores between 300 and 619 accounted for 61% of BNPL loan originations in 2025).

The Hidden Threat to the Economy

A single BNPL loan won’t crash the economy but millions of them might. The greatest danger isn’t a financed DoorDash order. It’s conditioning an entire generation to misunderstand debt, while believing affordability is measured by the installment payment amount instead of the total price.

First, BNPL is creating shadow debt in the economy.

Much of this borrowing sits outside traditional credit reporting – leaving regulators, banks, investors, and even borrowers without a complete picture of household debt. Every financial crisis has hidden leverage. In 2008 it was mortgage-backed securities. Tomorrow it could be hundreds of billions of dollars of installment debt quietly accumulating beneath the surface until consumers stop paying.

Second, BNPL artificially boosts consumer spending.

Retail sales look stronger. Company earnings look healthier. Consumers appear more resilient than they really are. But eventually tomorrow arrives. When households hit the payment wall, spending will slow, retail earnings will weaken, and layoffs will follow. What looked like sustainable growth can quickly prove to be borrowed demand. Stock prices and valuations will eventually be impacted.

Third, financial hardship rarely comes from one decision.

This time it will be death by a thousand installment payments. One installment payment for shoes. Another for groceries. Another for concert tickets. Then payday arrives and the money is gone as quickly as it arrived. Financial stress is contagious. When households struggle to pay one debt obligation, they often fall behind on other obligations.

Finally, banks aren’t the lenders this time – its Fintech companies.

Regulators spent the last 15 years demanding more capital, more transparency, and tougher stress tests for banks. Meanwhile, an entirely new lending industry emerged with fewer rules, lighter oversight, and limited visibility into the risks building beneath the surface. We’ve seen this movie before. Regulation usually arrives after the damage is done.

What It Means for Your Money

If this is really the early stage of another debt bubble, now is the time to prepare not panic. Here are some quick tips for what you should do:

If you are using BNPL products, start to use them in a disciplined manner. Follow these tips that I previously shared.

Treat BNPL exactly like any other loan or debt.

Avoid debt stacking - taking on multiple installment loans at once.

Eliminate or lower your total amount of high-interest debt.

The Bottom Line

Today’s BNPL market is a fraternal, not identical, twin to the subprime mortgage market. Every financial bubble begins with the same lie: “This time is different.” We once convinced ourselves that anyone could afford a house because home prices would never fall. Today we’re convincing ourselves that anyone can afford anything as long as the monthly payment is small enough.

Debt does not become safer because the marketing team replaces the word ‘loan’ with ‘4 installment payments.’ America is once again fueling economic growth on money lent to the most financially vulnerable. We ignored the warning signs of a crisis once before. The online checkout cart may be where the next one begins.

About the Author: Femi F. is the Founder of Hustle & Finance and a personal finance expert. He is a disciplined student of markets, money habits, and long-term wealth creation. Femi combines institutional-level market expertise with a culturally relevant, real-world approach to wealth building. His principals are based on living your best life today, while managing your money responsibly for tomorrow.

Disclaimer: This article is intended for educational and informational purposes only and should not be construed as financial, investment, legal, or tax advice. The views expressed are solely the author’s opinions and are not recommendations to buy, sell, borrow, invest, or take any specific financial action. Financial decisions should be made based on your individual circumstances, risk tolerance, and consultation with a qualified professional. Readers are solely responsible for any actions or decisions they take based on this content. Neither the author nor the platform assumes any liability for losses, damages, or outcomes resulting from the use or application of any information, opinions, or strategies discussed. Use of Buy Now, Pay Later products and other forms of consumer debt carries financial risk, including fees, interest charges, and potential impacts to your credit profile.